4 Ways to get your business audited by the IRS

Tax season is shifting into high gear. This is also the time of year we are most likely to think about the potential of being audited by the IRS. Even though the potential for an Audit is only about 1% for business owners, the simple math says out of 100 of your business peers at least one of you are going have more intimate relationship with the IRS this year.

For many business owners tax season is viewed as a dreaded time of the year when they are forced to sit down with their CPA and begrudgingly discuss the numbers of their business. It should be noted our experience shows that businesses that meet more regularly with their CPA’s (at a minimum quarterly) have a much better handle on the finances of their business. That discipline would be referred to as Tax Planning. Tax Planning is a good thing; it is legal and highly recommended. If your business has any level of complexity, seeking consultation from a tax professional is always good advice. However, it’s sometimes tempting counterpart, Tax Evasion is another; Tax evasion is deliberately misrepresenting the state of your affairs to the IRS.

Improper tax accounting is usually not viewed as tax evasion unless the IRS determines there was fraudulent intent by the business owner.

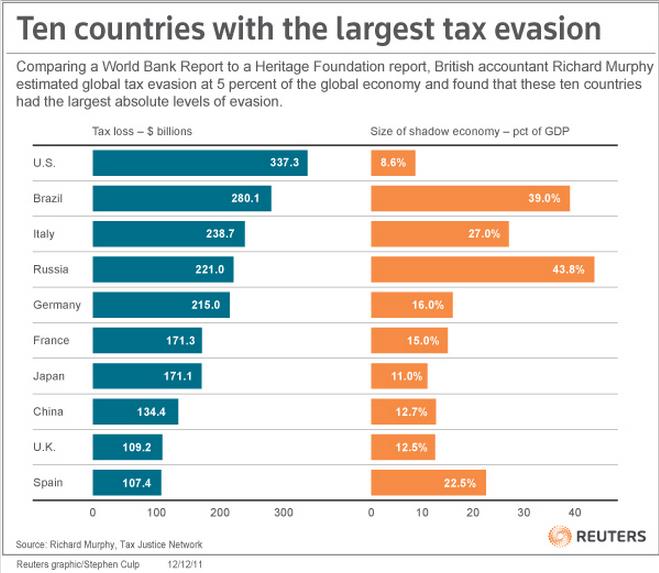

In 2011, British accountant Richard Murphy estimated global tax evasion to be 5% of the global economy. The USA led the way with 337.3 billion. But because the US is the largest global economy, the amount as percent of GDP, was only 8.6%; the lowest of the top 10 countries. So I guess as American Business owners, you can pat yourself on the back for that statistic! Regardless of size, at its core, any number above 0% says something about the overall moral fiber and principles being practiced.

With those numbers in mind, here are 4 discrepancies the IRS has been known to target should this be the year you are part of the 1% of audited businesses.

1) Discrepancies in Accounting.

- The amounts on the financial statements should match what is on the corporations return.

- Any irregularities raise questions.

2) Not reporting significant amounts of Income.

- Business owners not accurately reporting business receipts.

- Shareholders not reporting dividends they pay themselves.

3) Deduction Claims

- Grossly overstating travel expenses

- Fictitious deductions

- Stating personal expenses as business expenses

- Overstating charitable contributions.

- Lack of Verification

4) Improper distribution of income

- An example of this would be a stockholder directing income to a lower income bracket family member(s) to reduce their tax liability. (paying the kids)

The list above is not meant to be a complete list. It would be logical to assume that during an audit, if something is uncovered that doesn’t add up, the auditors will naturally dig deeper in the area of the discrepancy. And the goal of this post is not to sound like a tax expert, but to remind you as a business owner this is serious stuff and it should not be taken lightly.

Have you ever been audited? If anyone has some additional thoughts on this subject, please share them in the space below. Without a doubt as business owners this is a common thread that binds us all so your input and suggestions would be greatly appreciated.

Chris Steinlage Kansas City Business Coach

Photo by JD Hancock via Flickr